How Far Will House Prices Fall and How Quickly Will They Rise?

In recent times we have seen a lot of negativity surrounding house prices. Not only have house prices already fallen 4% from their peak last year, but there is greater fear that The Bank of England will have to keep increasing interest rates, causing a squeeze on the affordability of buyers. There is also a complete reversal in the trend of their being more buyers than sellers and nowadays this is clearly the other way round. Lets look into the data and what is currently happening in the housing market.

Inflation and Interest Rates Affecting the Cost of Mortgages

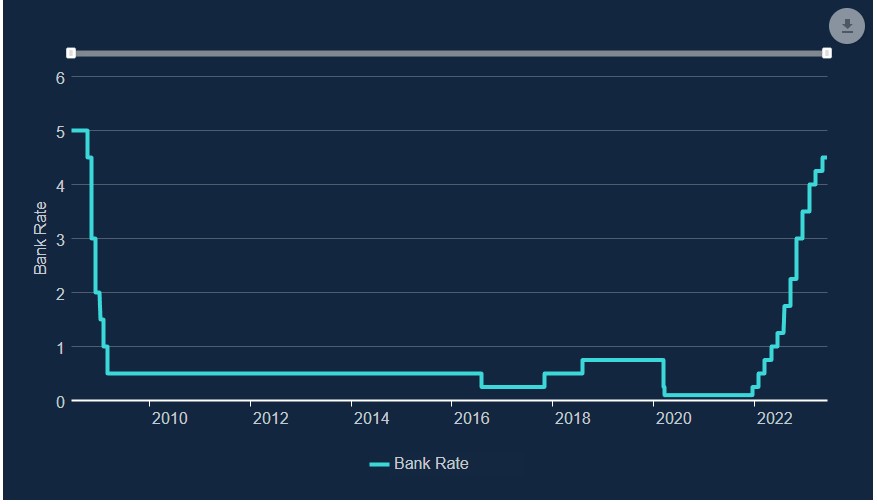

In April it was reported by the ONS that Food prices increased 19.1%, in March this figure was slightly higher at 19.2% so on a month on month basis the food inflation situation remains unchanged. It was expected that the rate of inflation would be under control by now but it’s not. We are now at a point where inflation has risen at the fastest rate in 45 years. More alarmingly Core inflation is currently 6.8% the highest rate since 1992. Because of this It is expected that the Bank of England interest rates could go higher due to their current lack of control on the rate of inflation.

With higher interest rates more current mortgage holders will feel the financial pinch and more prospective buyers will be unable to buy a house at a higher price than when interest rates were lower. The lack of house buyers and the lack of affordability could cause house prices to fall further.

Mortgage Approvals are Already Lower

Recent figures show that 48,000 mortgages were approved in April and if you compare this to figures seen in 2020 you can see there was a lot more demand from house buyers and mortgage approvals were around 100,000 per month. There are now over 50% less buyers who are completing property purchases and less demand for properties will bring prices down. Gone are the days when people were overpaying for houses and offering above the asking price, nowadays properties are completing at a discount to the asking price.

The Amount of Properties Being Offered for Sale are Significantly More

When looking at the amount of house listings being offered on Rightmove it can be seen that at the beginning of the year there were around 230,000 listings and now this is above 400,000. The property market is clearly in a situation where there are far more sellers than buyers. many people may be more concerned to sell their house fast due to the fear of house prices falling further. those sellers will need to reduce their asking price to compete and attract a buyer from the ever decreasing pool of buyers.

How Far Will House Prices Fall?

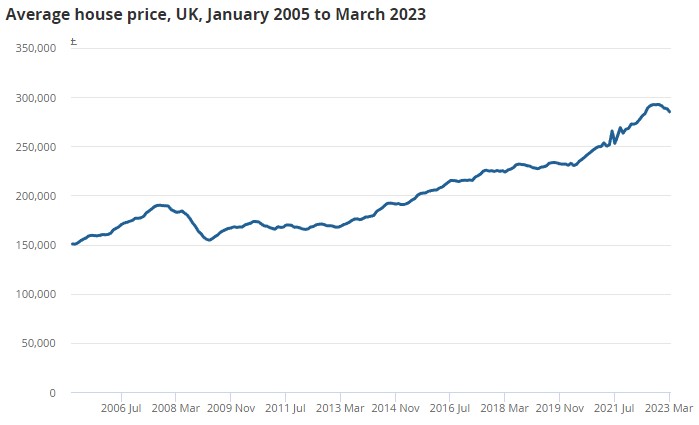

In February 2023 on The Martin Lewis Money show, Andrew Wishart, a housing market analyst at Capital Economics gave some house price predictions. Andrew stated that house prices have already fallen 4% from their peak that was seen in the summer of 2022. He predicts that house prices will fall another 8% bringing the total fall in house prices to being 12% and it is expected that this will bottom out towards the end of the year. In the recession of 2008 it is said that “UK average house prices fell as much as 21% during the recession after the 2008 crisis, as can be seen here.

When Will House Prices Rise Again?

Andrew Wishart says that he believes that after prices bottom out at the end of 2023, House prices will remain stagnant during 2024 and we could expect to see house prices rising again in 2025. It is however noted that his views on how far house prices will fall and how long the dip will last is more pessimistic than other analysts. At Direct House Buyer we believe that the market will bottom out quicker than the end of the year possibly around August and the fall may be a further 6. Take for example the property crash of 2008 after a similar drop to what we have recently seen, house prices took a steep decline which lasted around 7 months. Things always seem to happen faster than expected these days.

Will Rental Prices Keep Increasing?

In the show Andrew believes that we are already past the fast rise in rental increases that we have experienced during the pandemic. However, with mortgage rates currently being so high and therefore less people able to get onto the property market, demand for rental properties will still remain high. Furthermore, landlords are also experiencing higher mortgage rates and they will likely have to pass this extra cost onto the tenants.

We are currently seeing far less rental properties coming onto the market and a scramble of renters needing to find a property. This high demand is causing rental prices to rise as Landlords realise that there isn’t much competition and renters are finding themselves in a ever increasing desperate position.

Changes in policy is also forcing landlords to sell their house and this could only result in their being less properties available to rent.

How Much Higher Will Interest Rates Go?

The Bank of England further increased the base interest rate another 0.5% to 4.5% bringing interest rates to a 15 year high. This will further increase the costs of living for the UK population and will result in less money being spent in stores. The Bank of England have stated that their aim is to keep inflation at 2%.

The incremental rise in interest rates that we have seen since January 2022 now results in an extra expense of around £200 monthly payment for every £100,000 of mortgage debt.

Santander has said that 400,000 of its mortgage holders are due to have their fixed mortgage rates expire in the near term. On average this will add £313 to their customers mortgage payments each month, when combined with the increase in energy bills we may see a lot more mortgage defaults and repossessions later in the year. In Santanders full year accounts it shows that “the lender put aside £321m in 2022 to cover potential defaults“.

Andrew Wishart says the consensus is that we may just see one more 0.5% Interest rate hike and it seems that the Bank of England are coming to an end of raising interest rates. Interest rates will remain the same for the rest of the year and will fall back down to 3% by the end of 2024. These rises have already started to work on tackling on inflation and once that’s achieved there will be no reason to continue raising interest rates.

Should you choose a 5 Year Fixed Mortgage or a Two Year Fixed Rate?

If house prices are predicted to bottom out at the end of the year then many new house buyers will have the opportunity to buy a house at a good price. If it is predicted that Interest rates will possibly start to fall during 2024 then by fixing in a 2 year rate, buyers will have to pay more than a 5 year rate initially but they will then be able to switch to a cheaper mortgage rate once their 2 year term comes to an end.

What Does The UK Population Think Will Happen to House Prices?

During the money show they conducted a poll asking the UK Population if they think house prices will be higher or lower in your area in a years time the results were:

- Higher 32%

- Roughly the Same 38%

- Lower 27%

- 3% Don’t Know

These results are surprisingly different to what market analysts believe and Martin Lewis explains that people often have a general belief that the area they live in is different to what happens to the rest of the property market. This positive sentiment will make a difference and will provide more confidence for people who want to buy a house. Andrew Wishart said as more people realise that house prices are coming down the current positive sentiment from The UK population will also decrease.

Nationwide Have Reported Falling House Prices for 7 Months in a Row

Nationwide have reported falling house prices for seven month in a row and only showed a small increase in April but in May’s figures we have returned to another fall. It’s inevitable that the Land Registry figures which are a couple of months behind will catch up with reporting similar data showing a strong trend of falling house prices.

Due to the Government being unable to tackle inflation as quick as they hoped it is now expected that interest rates will rise higher than predicted and remain unchanged for a longer period of time time. Therefore, a crash in property prices may continue for longer than expected.